Article

Satellite-terrestrial convergence, why satellites and mobile networks are merging into one infrastructure

Satellites and mobile networks are converging into a single hybrid infrastructure. The question now is who will control its critical layers, from spectrum and devices to the ground segment and the customer

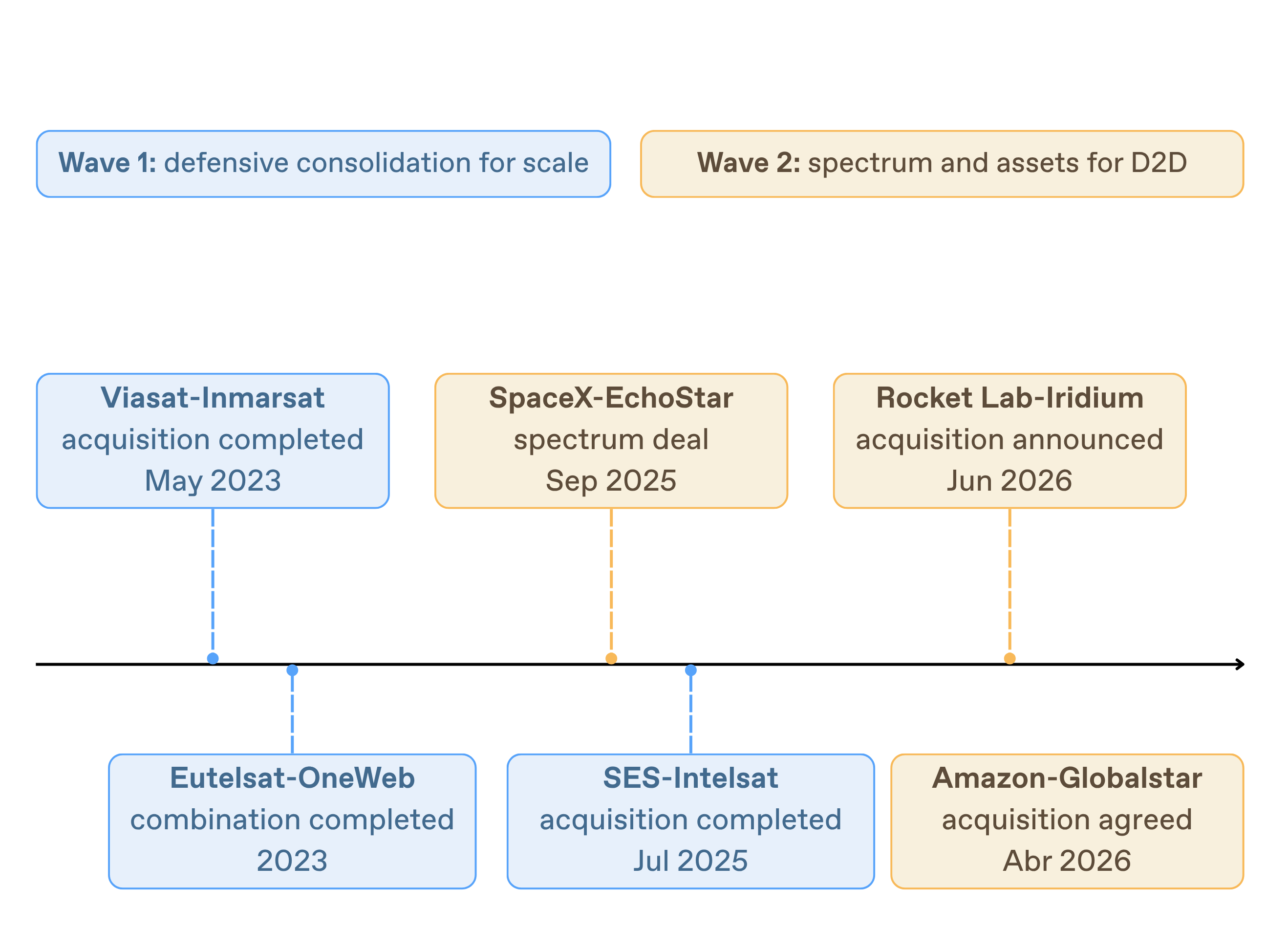

$36 billion in one year, why satellite M&A is booming

In the span of a year, the satellite market has seen an unprecedented run of corporate activity. Deals announced or agreed by players like Rocket Lab, Amazon, and SpaceX all point in the same strategic direction. They are locking up spectrum, customer access, launch capacity, and integration with mobile networks.

Three deals, more than $36 billion, and one underlying pattern. The first wave of satellite consolidation (Viasat-Inmarsat, SES-Intelsat, Eutelsat-OneWeb) was largely defensive, a play for scale against the decline of the broadcast business and the pressure of the low-cost LEO model. This new wave is different. Nobody is buying satellites anymore. They're buying spectrum, customer access, launch capacity, and integration with mobile networks. What these deals have in common isn't space. It's control of the layers that will turn satellite connectivity into a true extension of the mobile network.

The classic strategic question was who owned the satellites. The new one is different. Who controls the layers required for convergence? Spectrum, mobile operator alliances, device compatibility, launch capacity, LEO/MEO/GEO assets, ground segment, cloud integration, regulatory approvals, and customer ownership. Whoever controls several of these layers, or knows how to orchestrate them, will hold the advantage for years.

What is satellite-terrestrial convergence?

Satellite-terrestrial convergence is the integration of satellite networks and terrestrial telecommunications networks (mobile and fiber) into a single hybrid connectivity infrastructure, where the same device, the same user identity, and the same network core operate seamlessly over terrestrial or satellite access.

For decades, satellite communications were a world apart. TV broadcasting, maritime communications, government, remote connectivity. Terrestrial networks, meanwhile, were built on towers, fiber, licensed spectrum, mobile cores, and a direct relationship with the customer.

That separation is now breaking down, driven by three forces acting at once.

LEO megaconstellations, which have cut latency enough to make broadband-class services viable.

Demand for universal connectivity in territories where terrestrial networks don't reach or don't pay off.

Resilience, now a hard requirement for public safety, energy, logistics, banking, and government operations.

5G NTN, the standard that makes satellites part of the mobile network

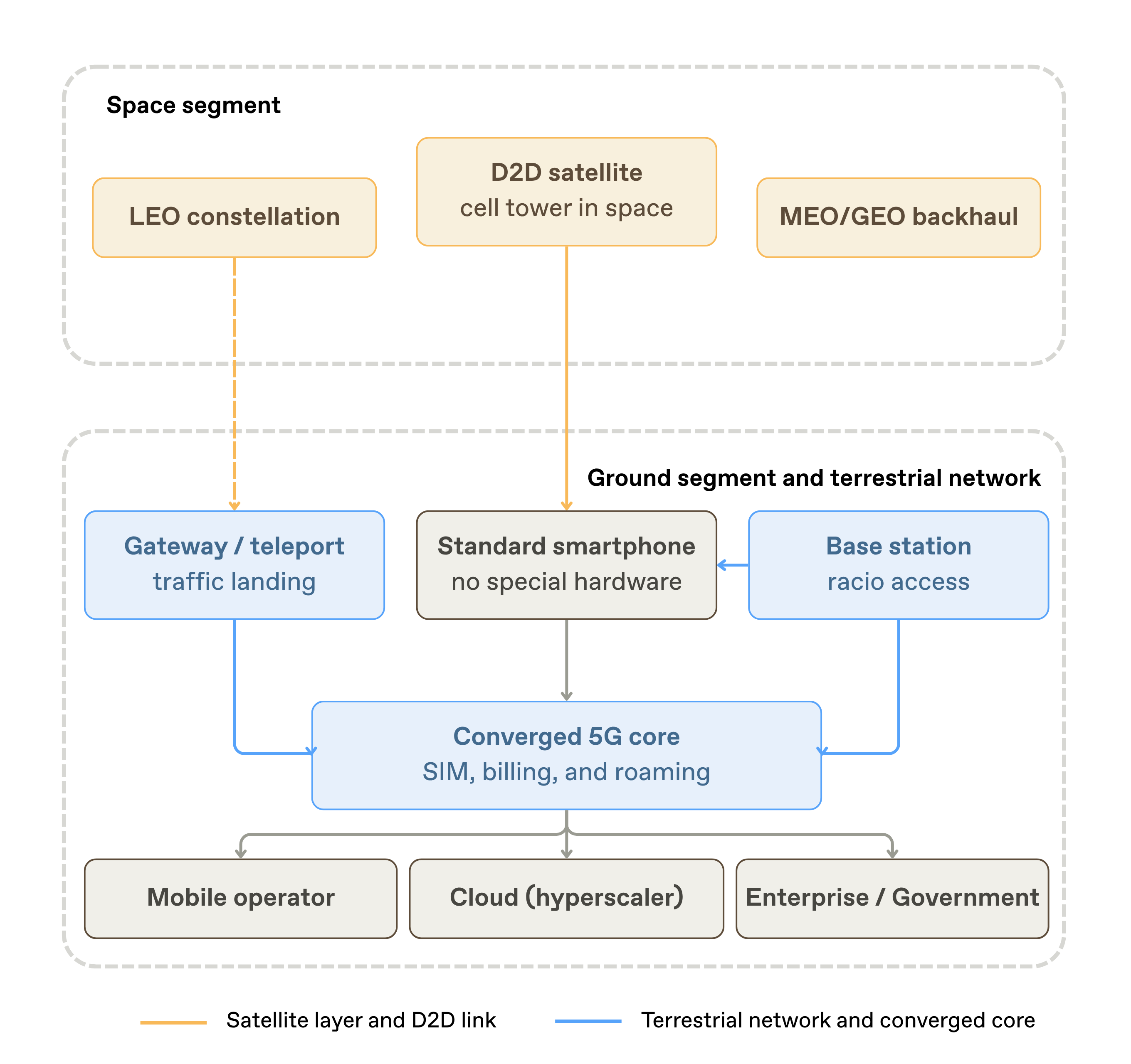

The technical foundation of convergence is 5G NTN (Non-Terrestrial Networks), the set of 3GPP specifications that integrates satellite access into the mobile architecture, from roaming between terrestrial and satellite networks to satellite backhaul into the 5G core. In practice, the satellite stops being a parallel service and becomes part of the mobile network itself.

What is direct-to-device (D2D) and how does it work?

Direct-to-device (D2D), also known as direct-to-cell, lets a standard smartphone connect directly to a satellite, with no dish and no specialized terminal. The satellite effectively acts as a cell tower in space.

The first mass-market case was Apple's emergency messaging over Globalstar's network. Today, Starlink already offers commercial satellite messaging for 4G phones in markets like the United States and New Zealand, with a roadmap that runs from messaging to IoT and, further out, voice and limited data.

D2D is not a satellite product. It's a telecommunications product. It depends on mobile spectrum, devices, operator agreements, roaming, regulatory approvals, and customer integration.

Two complementary paths coexist. On one side, today's commercial D2D overlay, which scales fast because it leverages existing smartphones and existing relationships with mobile network operators (MNOs). On the other, standardized NTN, which will be natively integrated into 5G Advanced and 6G architectures. They aren't mutually exclusive. The likely outcome is a hybrid model, with fast commercial services today and increasingly standardized architectures tomorrow.

Satellite spectrum, the bottleneck for direct-to-device

In D2D, spectrum is the barrier to entry. A smartphone has a small antenna and limited transmit power, which makes low and mid bands far more valuable for direct connection, especially L-band (1,000-2,000 MHz), S-band (2,000-4,000 MHz), and certain terrestrial mobile bands like 700 MHz and 800 MHz. Ku-band (12-18 GHz) and Ka-band (26.5-40 GHz) are excellent for environments that can carry larger antennas, such as broadband terminals, aircraft, and ships, but they're unworkable for a direct link to a conventional phone.

MSS spectrum (mobile satellite service) takes on special value here. It's one of the few reserves of satellite spectrum already aligned with mobile services, and therefore directly usable for D2D.

In Europe, the MSS strategy is taking shape around the harmonized 2 GHz band (1980-2010 MHz uplink and 2170-2200 MHz downlink), whose current authorizations expire in 2027. The European Commission is proposing a new EU-level selection procedure to avoid country-by-country fragmentation and bring greater industrial and regulatory coherence to how this spectrum is used.

For Europe, the goal goes beyond renewing licenses. It wants MSS to power D2D services, IoT, critical communications, resilience, and digital sovereignty. How it ultimately fits with initiatives like IRIS² will depend on how Europe combines commercial use, secure government capabilities, and coordination with mobile operators.

In parallel, CEPT is drawing a clear line between two regulatory paths. D2D over MSS bands can build on an existing framework, while D2D over terrestrial mobile bands will require more technical work, coordination with mobile operators, and new coexistence rules.

This centrality of spectrum explains the logic behind the recent M&A. Satellite operators with legacy businesses under pressure become strategic assets because of their spectrum. And the reverse holds too, since owning thousands of satellites without D2D-relevant spectrum forces you to buy or to partner. Spectrum has become the asset that organizes the entire board.

Will satellite operators buy mobile operators?

Most likely not, at least as a global strategy. Deeper integration can't be ruled out in specific markets, but mobile operators are expensive, nationally regulated, politically sensitive assets, and the economies of scale are limited in a business that remains deeply national.

The most likely model is alliance-based convergence. Satellite operators bring coverage extension; MNOs bring customers, spectrum, SIM authentication, billing, and core network integration; hyperscalers bring cloud, edge, and enterprise channels; and infrastructure owners bring ground stations, fiber, power, and regulated local presence.

Where the hybrid network adds value (and where it doesn't)

Satellite is not going to replace terrestrial 5G, and certainly not fiber networks. In dense urban environments, terrestrial networks will remain unbeatable on capacity and economics. A satellite beam covers an enormous area, which limits spectrum reuse; indoor coverage will remain a challenge; LEO satellites move fast and demand managing Doppler effects, beam steering, and complex handovers; and regulation advances country by country. These limitations define the thesis of convergence. Satellite doesn't replace terrestrial networks; it completes them.

The value lies in extension and resilience. It shows up in rural and remote areas where building towers doesn't pay off; in maritime and aviation environments; in emergencies and disasters, when the terrestrial network goes down; in massive IoT across agriculture, energy, logistics, and ports; in sovereign and mission-critical communications for enterprises and governments; and in solutions for mobile operators themselves, from rural backhaul to temporary coverage and premium resilience services.

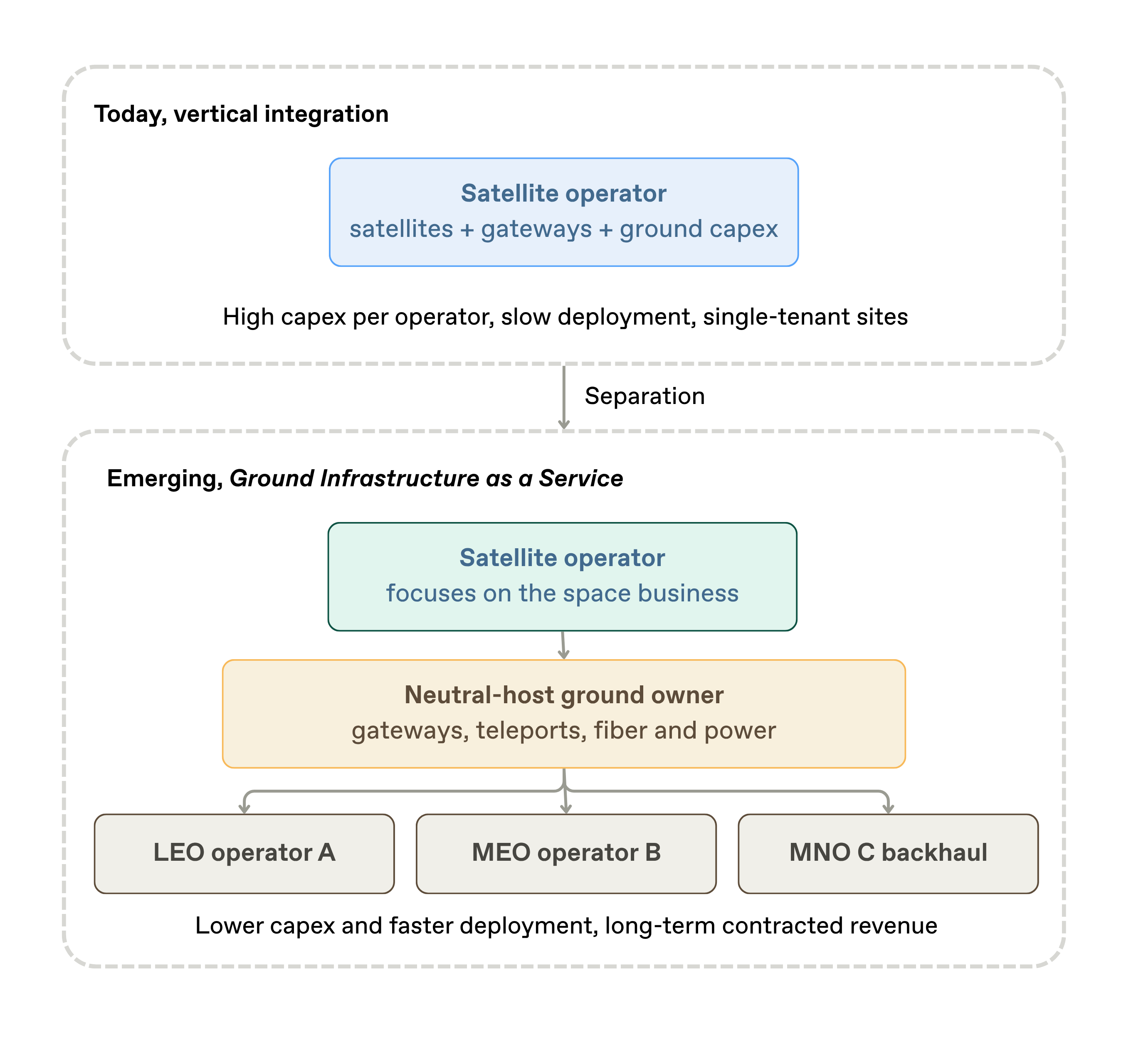

Ground Infrastructure as a Service, the ground segment opportunity

There's one piece that still gets little attention, the ground segment. LEO constellations need gateways, teleports, cloud interconnection, backhaul fiber, national landing rights, and resilient power. Ground stations are where space networks meet terrestrial ones.

A Ground Infrastructure as a Service model is starting to take shape, and it echoes the history of towers. Mobile operators owned their towers until those towers became a multi-tenant, neutral-host asset class. That same separation is now beginning to happen in the satellite ground segment.

The satellite operator cuts capex and speeds up deployment; the infrastructure owner locks in long-term contracted revenue, an anchor tenant, and a multi-tenant runway.

For TowerCos, fiber operators, data centers, and infrastructure funds, the ground segment is a natural extension of their business, with critical physical assets, long-term contracts, anchor tenants, and multi-tenant potential. The terrestrial side of satellite convergence could end up being worth as much as the space side.

What satellite-terrestrial convergence means for each player

For mobile operators, the priority will be using satellite without losing the customer relationship. That can take the form of a bundled service, a premium add-on, an enterprise product, a wholesale agreement, or a tool for meeting coverage obligations. In Europe, and in Spain in particular, this has stopped being theoretical. Meeting rural coverage commitments and keeping communications running through an emergency (a lesson seared into memory here after recent episodes in which network outages made the crisis worse) are now business arguments, not just regulatory ones.

For satellite operators, the challenge is moving from capacity vendors to integrated connectivity partners. Winning will depend less on the satellites and more on spectrum strategy, MNO integration, device compatibility, enterprise channels, and the ground segment.

For TowerCos and digital infrastructure investors, convergence opens up a new asset class, and few markets are better positioned to lead it than Spain, a European powerhouse in towers, fiber, and neutral-host assets.

For hyperscalers, satellite extends the reach of the cloud, strengthens edge resilience, and opens new enterprise networking propositions, with the cloud-native satellite network acting as an extension of global cloud infrastructure.

For governments and regulators, the challenge is balancing innovation, competition, spectrum protection, emergency resilience, and sovereignty. The winners won't be those with the most satellites, but those with the clearest regulatory and industrial strategy. Europe knows it. IRIS², its third flagship space program, is the institutional response, a multi-orbit constellation built for secure connectivity for government users. But sovereignty won't be solved by public programs alone. It will require commercial D2D strategies, harmonized spectrum positions, MNO-satellite alliances, and ownership of the ground segment.

For Spain, geography settles the argument. A depopulated interior, island territories, a vast maritime domain, and ports that serve as gateways for global trade make the hybrid satellite-terrestrial model not one option among several, but the only architecture that makes sense. If the network of the future is hybrid, European and Spanish sovereignty will have to be hybrid too.

One hybrid infrastructure

The question is no longer whether satellite and terrestrial networks will converge; they already are. The real question is what role each player wants to take, whether owner, partner, orchestrator, regulator, investor, or customer. It's a decision about operating models, regulation, and business strategy, and it's where Nae works alongside operators, infrastructure managers, public administrations, and investors, from spectrum strategy and digital infrastructure business models to the governance of large-scale deployments.

The future won't be terrestrial or satellite. It will be one hybrid infrastructure, terrestrial where density matters, satellite where reach and resilience matter, and convergent wherever the customer simply expects their connection to work, wherever they are.